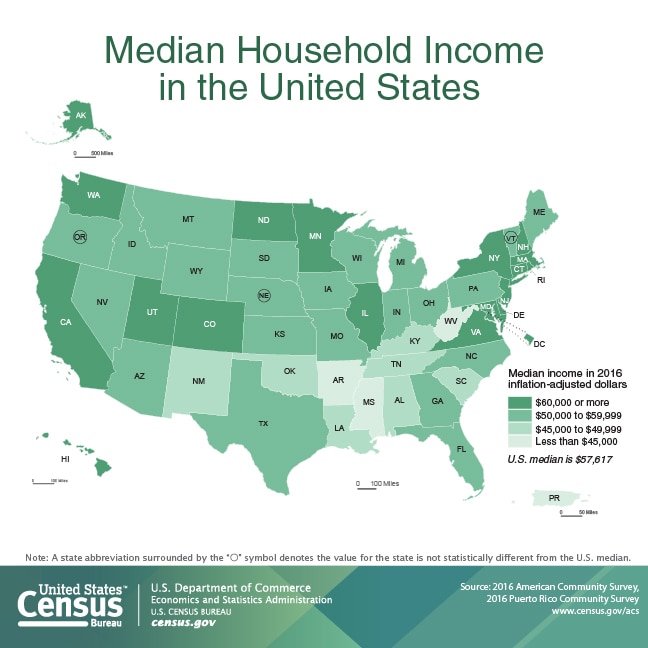

Did you know that $57,617 is the line separating top earners from bottom earners in the US? Or at least it was, in the 2016 Census Bureau survey of median household income in the country.

{kind=link}

So… How do you or your household compare? Does your income fall within or under the median worker wage of $44,564 a year? If so, then you may be thinking that you’re not doing that well.

Not always, because it also depends on where you live. There’s also how you balance fixed expenses with disposable income and still get to put away savings.

That’s right. Even as someone living on a fixed income, you can still take care of all your financial responsibilities and save at the same time!

But it all boils down on how you budget your income.

Don’t worry. If you have no idea how to, we’ll show you the way!

1. Know What Your Fixed and Variable Expenses Are

To answer your question of how to budget income, you first need to know what your fixed expenses are. As well as your variable expenses.

As the term suggests, these are expenses which amounts don’t change. They stay the same, whether you pay for them every week, month, or year.

If you have a fixed-rate mortgage, then that’s a perfect example of fixed expense. The same goes true for your rental payments, car loan payments, insurance premiums, and fixed rate phone services. Paying off your personal loans, say every month, can also be a type of fixed expense.

Variable expenses, on the other hand, are expenses that have varying amounts. They can either fall under “discretionary spending” or necessities.

Examples of the former include clothes shopping, dining out, or going to the movies. Groceries, utility bills, transportation, refilling your car’s fuel tank, and maintenance are necessities.

Fixed expenses, seeing that they don’t change, makes them easier to create a budget for. It’s the variables that pose a more serious challenge. But budgeting for the discretionary spending and necessities is still doable!

2. Calculate All Sources of Income

Say you don’t have a family yet, which means your income is all you depend on. But you have a fixed income and you also make some more on the side (maybe you sell made-to-order baked goodies or you have a woodwork shop).

However, unless you have a regular stream of clients, focus on your primary income first. You need another budgeting model for your variable income.

3. Deduct Your Fixed Expenses from Your Fixed Income

Ever heard of the saying “Compare apples to apples and oranges to oranges” approach? Apply the same thing when you budget income. That means you first need to subtract your expenses with fixed amounts from your fixed salary.

Here’s an example using the average mortgage payment of borrowers in December 2016, amounting to $758.

$3,714 (above-mentioned median wage divided by 12 months) less $758 means you have $2,956 left after a mortgage payment for that month. Now, keep subtracting the rest of your listed fixed expenses from this.

Take note of the total, since you’ll use it to figure out how to budget your variable spending after.

4. Factor in Your Variable Expenses

Next, list all of your variable expenses. That includes all utilities and services, groceries, gas or transportation expense, restaurant meals, shopping, and recreation.

It’s best you make them as detailed as possible since you’ll have an easier time making accurate estimates for them.

5. Deduct Your Most Recent Variable Expenses from Your Fixed Income

Once you’ve totaled your typical variable expenses, subtract it from the fixed income (less the fixed expenses already). This’ll show you how much more disposable income you have left and how much you can set aside for emergency funds and savings.

6. Plan for Appropriate Adjustments to Your Variable Spending

Listing all your variable expenses one by one also gives you an insight as to how much you’re spending on them. It’s easy to forget that you went through $50 for that night out with friends. Or that you went a little beyond your budget for that dress and ended up spending $70 instead of only $40.

From here, look at each expense and see where you can make adjustments. For example, you noticed your electricity bill went up to $130, well beyond the U.S. average of $112.59. It’s possible you tend to forget turning off all appliances and lights not in use, or that you’ve grown more dependent on your air conditioner.

In any case, there are ways to bring down your energy consumption, so do them to save on electricity costs. Do the same for the rest of the items on your variable expense list.

You’ll find it easier to use online calculators to figure out how much fraction or percentage you need for these adjustments.

What’s important is to set a realistic goal. You don’t want to be too stingy, or you may end up compromising your convenience, comfort, and quality of life.

7. Incorporate Emergency Funds and Savings into Your Budget

At this point, you already know how much money you have left from your income less all types of expenses. Give yourself some leeway, say $150 to $200 for unplanned personal spending. The rest, divide into what will go towards your lifestyle decisions and long-term savings.

A good plan to follow when organizing finances, especially a low income budget, is the 50/20/30 approach. In fraction form, that means 1/2 of your income goes towards fixed and expenses and necessities. The other half, you divide by five, 3/5 of which goes towards your lifestyle and the remaining towards savings.

For example, $3,714 divided by 2 (or 1/2 ) is $1,857. Reserve that for expenses. Then, take 3/5 of the remaining $1,857, which is $1,114.2, for your lifestyle choices. At the end of the month, you should have 2/5 left of the $1,857 or $742.80 for savings.

Start Budgeting Now to Build Savings

Imagine how knowing fixed expenses can lead to a savings of $740 a month, or $8,880 by the end of the year! That’s 8 to 9 times more than 69% of consumers in the U.S. have saved up! Having savings also give you better peace of mind, knowing that you have something to use in case of an emergency.

Want more money-saving tips like this? Visit our blog then! We have more useful financial strategies waiting for you there.